Navigating the Perils of Loan Scams in the USA: A Comprehensive Guide

In an era where financial pressures mount due to inflation, job instability, and unexpected expenses, millions of Americans turn to loans for relief. However, this vulnerability has fueled a surge in loan scams, sophisticated schemes designed to exploit those in need. Loan scams involve fraudulent lenders or imposters who promise quick cash but deliver only financial ruin. These deceptions range from fake personal loans to manipulated mortgage applications, often leveraging technology like AI and robocalls to reach victims. As of 2025, the landscape is more treacherous than ever, with consumer fraud losses exceeding $12.5 billion in 2024 alone, marking a 25% increase from the previous year. Loan-related fraud, including personal and mortgage scams, ranks among the top threats, with reports of mortgage scam incidents skyrocketing 407% since 2022. This article delves into the types, mechanics, statistics, warning signs, prevention strategies, and recovery steps for loan scams in the USA, arming readers with the knowledge to protect themselves.

The Many Faces of Loan Scams

Loan scams manifest in various forms, each tailored to exploit specific financial needs. Understanding these types is crucial for recognition and avoidance.

One prevalent category is personal loan scams, where fraudsters pose as legitimate lenders offering unsecured loans for debt consolidation, medical bills, or emergencies. They often target individuals with poor credit, promising “guaranteed approval” without checks. In reality, victims pay upfront fees or share sensitive data, only to receive nothing. Similarly, payday loan fraud preys on those seeking short-term cash advances. Scammers use stolen identities or false information to secure funds, leaving the real account holders liable.

Mortgage loan fraud is another major issue, affecting homebuyers and refinancers. This includes occupancy fraud (claiming a property as a primary residence when it’s not) or income inflation on applications. In 2025, hotspots like California and Florida have seen elevated risks, with fraudulent applications potentially numbering in the tens of thousands quarterly. The Financial Crimes Enforcement Network (FinCEN) notes a sharp rise in such reports since 2002, often involving brokers and fabricated documents.

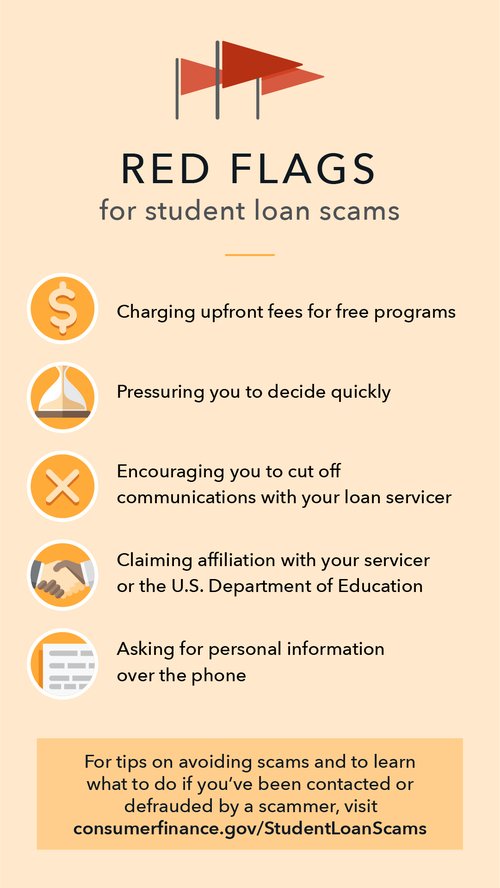

Student loan scams have surged post-pandemic, especially with repayment resumptions. Fraudsters impersonate servicers or government officials, offering “forgiveness” for fees. Robocalls claiming “Biden-approved” relief account for a significant portion of complaints, with loan-related calls comprising 21% of all robocall grievances in March 2025.

Auto loan fraud involves lying on applications for vehicle financing, while business loan fraud, including SBA and PPP variants, targets entrepreneurs. Though the PPP program ended, prosecutions for fake applications continue, with scammers inventing businesses to siphon funds.

These scams often intersect with broader fraud trends, such as AI-enhanced impersonations where voices or emails mimic trusted entities. In 2025, emerging threats include cryptocurrency-tied loan offers, blending investment hype with lending deceit.

How Scammers Operate: Tactics and Technology

Scammers employ a mix of psychological manipulation and cutting-edge tools to ensnare victims. The process typically begins with unsolicited contact—via phone, email, text, or social media—offering loans with attractive terms. In January 2025, Americans received over 4.7 billion robocalls, many peddling pre-approved loans. Spoofing technology makes numbers appear legitimate, building false trust.

Once engaged, fraudsters request personal details like Social Security numbers or bank info under the guise of verification. They may demand upfront payments for “processing” or “insurance,” often via untraceable methods like wire transfers, gift cards, or crypto. In imposter scams, which topped FTC reports, losses jumped dramatically, with government imposters alone causing $789 million in damages in 2024.

AI plays a growing role, generating realistic voices or chatbots to simulate lenders. Malware-laden apps, disguised as loan tools, steal data upon installation. Social engineering exploits urgency, pressuring quick decisions to bypass skepticism. For mortgage fraud, accomplices like appraisers inflate property values, enabling larger loans that default.

The endgame? Victims lose money directly or suffer identity theft, leading to unauthorized loans in their name. Scammers vanish, often operating from overseas, making recovery challenging.

Statistics and Economic Impact

The scale of loan scams in the USA is staggering. In 2024, total fraud losses hit $12.5 billion, with one in three reports involving monetary loss—a rise from one in four the prior year. Loan fraud ranks fifth among common fraud types, encompassing business and personal variants.

Mortgage-specific scams saw monthly reports climb from 14 in 2022 to 71 in 2025, a 407% increase, though only 12.24% reported losses. FinCEN data shows a surge in suspicious activity reports (SARs) for mortgage fraud, with 82,851 filed between 1996 and 2006, but trends indicate continued growth into 2025.

Online-originated scams caused over $3 billion in losses, surpassing traditional methods. Demographics reveal vulnerabilities: lower-income individuals and those with poor credit are prime targets, while states like New Hampshire report high per-capita fraud. The median loss per scam is $500, but phone-interacted frauds average $1,500.

Beyond dollars, impacts include credit damage, bankruptcy risks, and emotional distress. Lenders, facing losses, may raise rates or tighten criteria, affecting legitimate borrowers.

Spotting the Red Flags: Warning Signs

Courtesy of Consumer Financial Protection Bureau: Red flags for student loan scams, applicable to broader loan fraud.

Vigilance is key to avoiding scams. Here are ten common signs from experts:

- Guaranteed approval without credit checks.

- Upfront fees demanded before funding.

- High-pressure tactics to act immediately.

- Unsolicited offers from unknown lenders.

- Terms too good to be true, like ultra-low rates.

- Lack of contact info or professional website.

- No physical address provided.

- Unregistered in your state.

- Suspicious website (no HTTPS, poor design).

- Last-minute requests for wire transfers or account access.

Additional indicators include unexplained credit inquiries, micro-deposits in accounts, or debt collection calls for unknown loans. For banking-related loan scams, watch for phishing texts or emails mimicking lenders.

Courtesy of Synovus: How to spot red flags for banking scams, including loan-related fraud.

Prevention Strategies: Safeguarding Your Finances

Prevention starts with skepticism. Always initiate contact with lenders yourself, using verified sources. Research via searches like “[lender name] scam” and check state registrations through attorneys general.

Monitor credit reports weekly at AnnualCreditReport.com and use monitoring services for alerts. Enable multifactor authentication and avoid sharing info over unsolicited calls. For student loans, use official sites like StudentAid.gov.

Block robocalls with apps and report suspicious activity to the FTC at ReportFraud.ftc.gov. Consider identity protection services to detect fraud early. Never pay upfront or use untraceable methods.

What to Do If You’ve Been Scammed

Act swiftly: Cease contact, document everything, and notify your bank to freeze accounts. Report to the FTC, CFPB, and local police. Place fraud alerts or credit freezes via Equifax, Experian, and TransUnion. Seek refunds and monitor for further issues.

Conclusion: Empowerment Through Awareness

Loan scams thrive on desperation and deception, but knowledge is a powerful shield. By recognizing types, signs, and tactics, Americans can navigate financial needs safely. As fraud evolves with technology, staying informed and proactive is essential. Remember, if an offer seems too good, it probably is—verify, protect, and report to curb this epidemic.