Shield Your Finances Today!

In the fast-paced world of finance, borrowing money can feel like a lifeline – whether for a dream home, a new car, or simply bridging a gap until payday. But lurking in the shadows are unscrupulous lenders ready to exploit your needs. According to recent reports, scams have inflicted a staggering $64 billion in losses on Americans in 2025 alone, with lending fraud playing a significant role. Mortgage fraud, in particular, has seen median losses soaring to $371,818 per case. These deceptive practices not only drain your wallet but can ruin credit scores, lead to foreclosures, and cause long-term emotional distress. As the economy fluctuates, lenders – both legitimate ones bending rules and outright fraudsters – amp up their tactics to prey on the vulnerable. This article uncovers eight of the most insidious scams lenders perpetrate in the USA, arming you with knowledge to spot red flags and protect yourself. From predatory traps to hidden fee ambushes, we’ll dive deep into how they work, real-world examples, and foolproof prevention strategies. Stay vigilant; your financial future depends on it.

1. Advance Fee Loan Scams: The Upfront Payment Trap

One of the most blatant scams involves lenders demanding payment before disbursing any funds. These fraudsters pose as legitimate institutions, promising quick loans regardless of credit history. They’ll claim the fee covers “processing,” “insurance,” or “guarantee” – but once you pay, they vanish. In 2025, this tactic has evolved with sophisticated online platforms mimicking real banks, targeting low-income individuals desperate for cash. For instance, a New York resident reported losing $500 to a fake lender who required a “security deposit” via wire transfer, only to ghost them afterward. Signs include unsolicited offers, pressure to act fast, and requests for payment through untraceable methods like gift cards. To avoid this, remember: Legitimate lenders never ask for upfront fees. Always verify the lender’s registration with your state’s Department of Financial Services and check reviews on sites like the Better Business Bureau. If it sounds too good to be true, it probably is – walk away and report it to the FTC.

2. Bait and Switch: Luring with Low Rates, Delivering High Costs

Imagine seeing an ad for a 3% mortgage rate, only to find out at closing it’s jumped to 7%. This classic bait-and-switch scam hooks borrowers with attractive teaser rates that “expire” or don’t apply due to fabricated reasons like credit changes. Lenders might blame market shifts or undisclosed fine print, leaving you stuck with unaffordable terms. A California couple in 2024 fell victim, signing papers under duress and facing foreclosure within months. This scam thrives in competitive markets where borrowers rush without reading details. Red flags: Vague advertising, evasive answers about rate locks, or sudden “adjustments” post-application. Protect yourself by getting everything in writing, comparing multiple offers, and using tools like the CFPB’s rate checker. Insist on a Good Faith Estimate and consult an independent advisor before committing.

3. Predatory Lending: Targeting the Vulnerable with Toxic Terms

Predatory lenders zero in on minorities, seniors, and low-credit borrowers, offering loans with exorbitant interest rates, unnecessary add-ons, and terms designed to fail. Payday loans, for example, can carry APRs over 400%, trapping users in debt cycles. In Texas, regulators cracked down on a lender charging 600% interest to immigrant communities, leading to widespread defaults. These scams exploit desperation, often ignoring borrowers’ ability to repay – a violation of federal guidelines. Watch for aggressive sales tactics, loans exceeding 28% of income, or pushes for larger amounts than needed. Counter this by shopping around, understanding your rights under the Truth in Lending Act, and seeking free counseling from HUD-approved agencies. Building credit through secured cards can also reduce vulnerability to these sharks.

4. Loan Flipping: The Endless Refinance Cycle

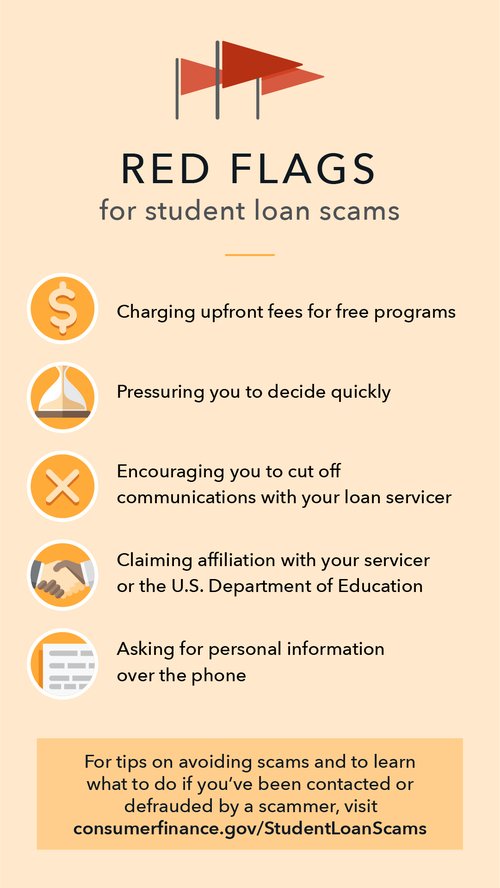

What are the signs of a student loan scam? | Consumer Financial Protection Bureau

Lenders encourage repeated refinancing to generate fees, even if it’s not in your best interest. Each “flip” resets the loan clock, adding costs and extending debt. A Florida homeowner was flipped five times in two years, accruing $20,000 in fees while barely reducing principal. This scam erodes equity and increases default risk. Indicators include unsolicited refinance offers shortly after closing or promises of “cash out” without clear benefits. Avoid by calculating total costs using amortization tools, waiting at least a year between refinances, and questioning any deal that doesn’t lower rates significantly. Federal laws limit excessive flipping, so report suspicious activity to the CFPB.

5. Equity Stripping: Draining Your Home’s Value

In this devious ploy, lenders approve high-loan-to-value mortgages or home equity lines, then encourage spending that strips away built-up equity. Combined with high fees and rates, it leads to underwater properties ripe for foreclosure. An elderly Michigan couple lost their home after a lender pushed a reverse mortgage laden with hidden costs, effectively stripping $150,000 in equity. Scammers target seniors via affinity groups or door-to-door pitches. Signs: Loans based solely on home value, not income; or add-ons like credit insurance. Safeguard by getting independent appraisals, limiting borrowing to essentials, and using equity calculators. Reverse mortgage counseling is mandatory – heed it!

6. Balloon Mortgages: The Ticking Time Bomb

These loans start with low monthly payments but end with a massive “balloon” lump sum. Lenders downplay the risk, assuming you’ll refinance – but if rates rise or credit dips, you’re sunk. A Georgia family faced a $200,000 balloon after five years, leading to forced sale. This scam preys on short-term thinkers in hot housing markets. Red flags: Unrealistically low initial payments or vague refinance guarantees. Prevent by opting for fixed-rate loans, stress-testing affordability for worst-case scenarios, and consulting financial planners. Always read the fine print on payment schedules.

7. Hidden Fees: The Sneaky Cost Accumulator

Lenders bury fees in complex documents – origination, underwriting, junk fees – inflating the true cost. A personal loan might advertise 5% interest but tack on 10% in hidden charges. In Illinois, a class-action suit exposed a lender adding $1,000 “administrative” fees post-signing. This erodes trust and balloons debt. Spot it through unclear disclosures or fees not itemized upfront. Combat by demanding a full Loan Estimate, comparing APRs (not just rates), and walking if anything feels off. Tools like Bankrate’s fee calculators help demystify costs.

8. Phantom Help: Fake Foreclosure Relief

During economic dips, scammers pose as “auditors” or relief experts, charging for services they never deliver. They promise loan modifications but pocket fees and disappear, worsening your situation. FTC data shows thousands affected yearly, with losses in the millions. A Nevada homeowner paid $3,000 for “forensic audits” that proved worthless. Warnings: Unsolicited calls, guarantees of success, or requests to stop paying your mortgage. Steer clear by using free government programs like Making Home Affordable, verifying helpers through HUD, and reporting to authorities immediately.

In conclusion, these eight scams highlight the dark underbelly of lending in the USA. With fraud losses hitting record highs, empowerment through education is key. Always research, seek second opinions, and trust your instincts. By staying informed, you can navigate borrowing safely and keep scammers at bay. Remember, legitimate lenders prioritize your success – if it feels wrong, it probably is. Protect your hard-earned money; your future self will thank you.